9:04 PM

9:04 PM

admin

admin

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

When the Fed announced QE III back in September it was difficult to determine just what was happening. QE should have been bullish for not only equities, which it wasn't - the S&P 500 (SPY) sold off 8.2% until the G-7 gave Japan the green light to devalue the Yen - but also Gold (GLD) which closed on Friday down 10.5% from the peak at $1800, putting in the lowest weekly close since the Euro bottomed back in late July. But the expansion of the Fed's balance sheet that was supposed to begin with QE III did not start taking place until the middle of December and the announcement of QE IV.

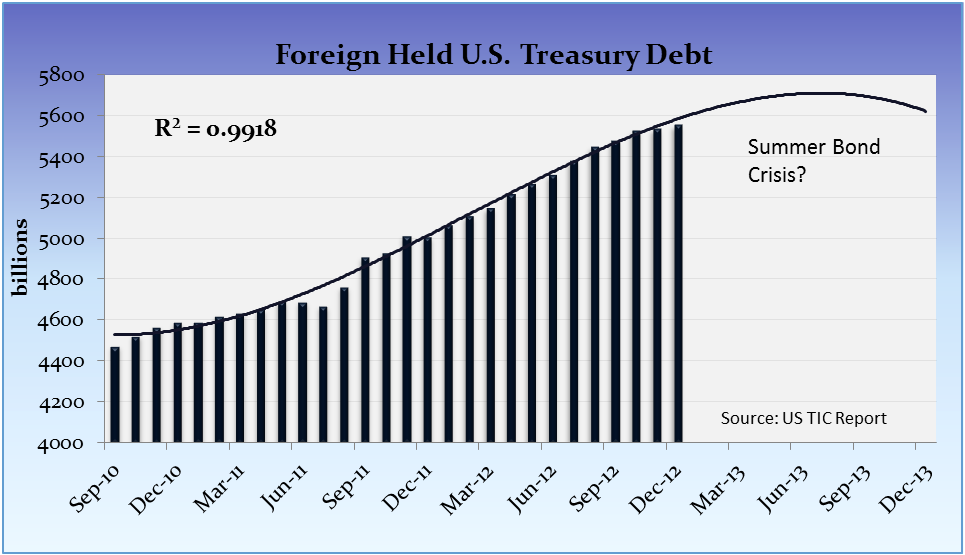

(click to enlarge)

The worry for the Fed has always been the day when the world would get its fill of U.S. Treasury securities. That would be the limit of the Dollar reserve system. To that end, therefore, watching the Treasury International Capital (TIC) report of Foreign Held Securities would clue us in as to whether we were approaching that day or not. The problem with the TIC report is that it is 60 days out of date, so our clues are always in serious hindsight. I've been building this chart for months and this third order polynomial fit is the best one of them all that represents a believable scenario.

Bondfall?

Looking at the latest data we can see that the rate of accumulation of U.S. treasuries by foreign central banks fell off sharply after the QE III announcement. The fear that has been held over our heads has beenwhat if China dumps its stockpile of U.S. Treasuries on the market, collapsing the Dollar?

The fear was real, because the Chinese had made a couple of major moves in that direction, spooking the markets.

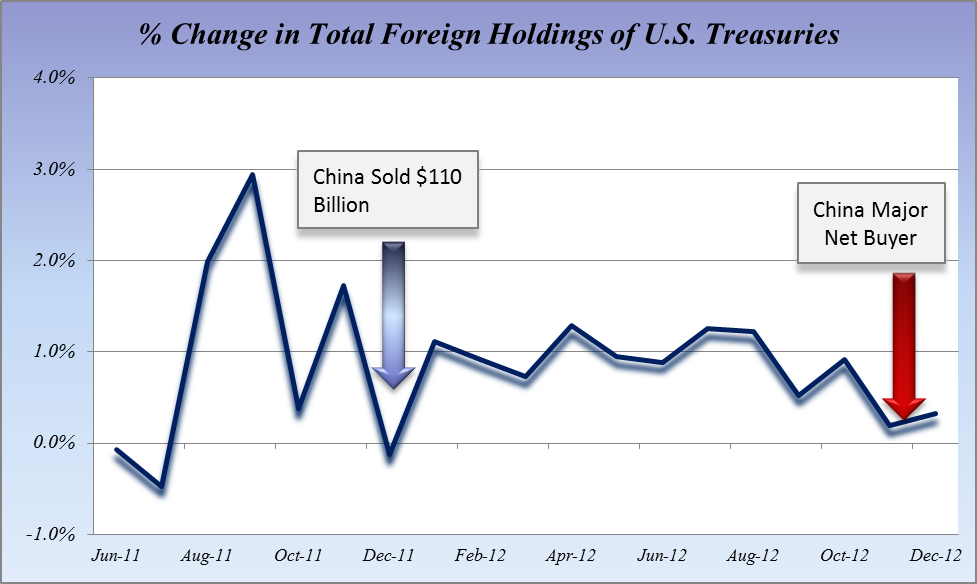

Between the end of QE II and the beginning of QE III the rate of foreign holdings rose steadily with the exception of two $100+ billion dumps by the Chinese. The first was in July 2011 and the second was in December. All through 2012 China was not a net buyer or seller of U.S. Treasuries with their holdings essentially flat until the announcement of QE III. One of the hallmarks of the TIC report is that the reported numbers are constantly revised month to month and it takes as much as 4 months for any one country's entry to stabilize. It wasn't until this month's report that the extent of the change in China's policy became apparent and the full extent of the irony of the situation along with it.

(click to enlarge)

Not only does the current TIC report show that the rate of accumulation of U.S. Treasuries slowed sharply in Q4, it reveals that without the mild buying by the Chinese there would have been net dishoarding by Foreign holders. In effect, it was China that stepped back into the role of international buyer of last resort starting in October. In November the TIC report rose $10.7 billion while China bought $13.2 billion. In December (latest data) the TIC rose $17.3 billion and China bought $19.3 billion. These numbers will change as the data is refined but the general point holds.

The Chinese Fed Trap

QE III was a program designed to force the Chinese to either let the Yuan appreciate significantly versus the Dollar or kick start their buying of Treasury bonds again. It seems that, on balance, the Chinese have chosen the middle path, doing a little of both as the Yuan has moved from ¥6.31 to ¥6.23 since mid-September.

This is one of the major reasons why bond yields across the spectrum are rising. When I wrote my article about the bond market's intraday collapse on February 1st, it was this kind of selling that I believed was going on in the background and why I felt that kind of selling was important. The action in the 30 year bond since then has been confirmatory with all rallies being sold and yields trapped between 3.14% and 3.23%. The Fed is obviously buying here to hold rates under control and it seems that they may still have an ally in China.

No one wants bond yields to rise too far too fast but everyone wants to offset the risk of inflation that the Fed is inviting by expanding its balance sheet dramatically. With the Fed promising zero interest rates for at least 3 more years - regardless of proclamations to the contrary - looking at bond yields below 3 years in duration is effectively meaningless. So, moving out to the 5 year note we see that yields began taking off in the U.S. 5 year note with the QE IV announcement.

This would be the lowest duration Treasury that has anything close to an open market and it has been pretty relentlessly sold. I have the German 5 year bond and spread up on the chart below to show that there hasn't been a rotation into Bunds as a safe-haven alternative. The money has rotated out of sovereign paper and European investors have been buyers of U.S. equities instead.

(click to enlarge)

This was certainly the case up until the devaluation of the Yen ceased. The Yen looks to have finished its move up and will likely trade in the ¥92 to ¥95 range to the Dollar and with that buying of German bonds has begun - widening spread to the 5 year UST. The Euro's rally has also taken a breather on a spate of poor economic data and the expectation that the ECB will have to begin expanding its balance sheet again.

But I wouldn't bet on that. The Chinese in the fourth quarter had to translate extra dollars into bonds to keep the Yuan from rising too quickly. In the 1st quarter, however, the strongly rising Euro likely provided a good sink for excess dollars as opposed to more treasuries. Given their history I would not bet on China taking on much more treasury debt without balking. They've made it clear how great their appetite is.

The Paper Tiger's Last Roar?

The Fed has expanded the monetary base by more than $200 billion in the last 6 weeks. Even if $90 billion of that are mortgage-backed securities, then the other $110 billion is Treasuries of all durations, far above the $40 billion per month that QE IV was supposed to be.

The adage has always been, "Don't fight the Fed." And, in the short term, I would agree with that. The brutal take down in gold and silver (AMEX:SLV) since January 22nd is proof of that. Since the Bundesbank issued its demand for the return of its gold, gold prices have been buried under an avalanche of paper even as the market gets pulled tighter. One has to wonder just how much of this is payback for that along with being an attack on the ECB's balance sheet. But, at this point it is hard to be a bond bull in the face of this amount of selling knowing what we now know of the shape of the market.

The early part of January was especially violent with major bond ETFs seeing huge single day redemptions. The iShares Barclays 3-7 Year Treasury Bond ETF (AMEX:IEI) saw $1.033 billion pulled out between January 2nd and the 4th - that's 33% of its AUM. But that's nothing compared to the ProShares Ultra 7-10 Year Treasury ETF (AMEX:UST) which went from an $800 million fund to a $19 million one in 5 trading days. So, as always, next month's TIC report will be full of interesting revelations as to where we were.

While you may not want to fight the Fed directly, I would be following everyone else who has begun quietly filing for the exits of the bond market.

please give me comments thanks

0 comments:

Post a Comment